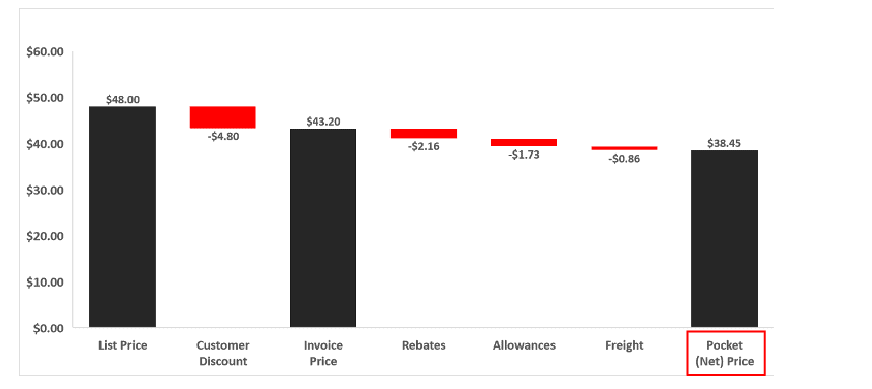

A price waterfall analysis is simply a visual breakdown of the revenue and margin a company makes from each of its transactions. Price waterfalls determine the actual price (referred to as Pocket Price or Net Price) charged to customers for each transaction and reveal hidden costs and leakages or deductions that erode margin (e.g. discounts, allowances and rebates).

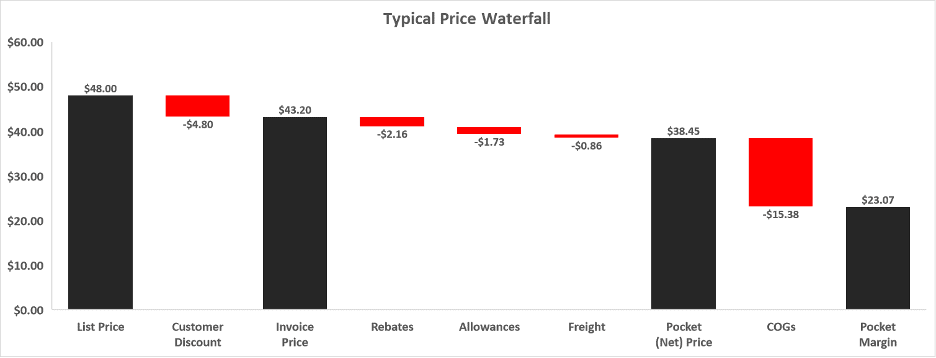

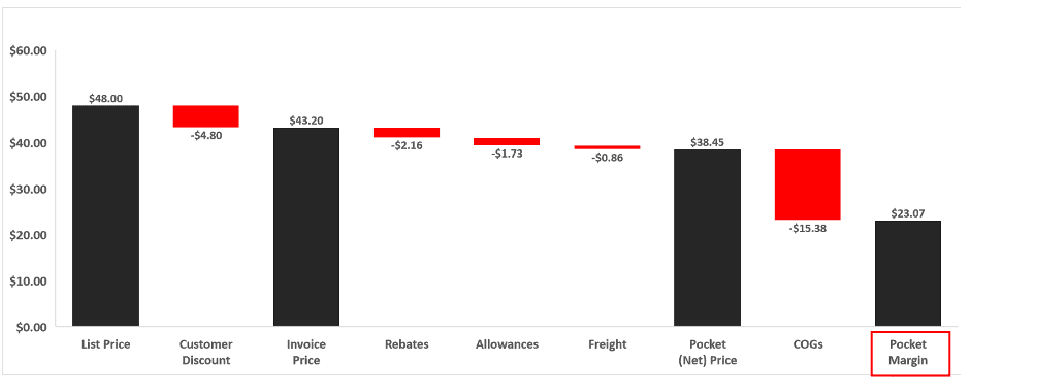

Below is an example of a typical price waterfall analysis.

We begin with the list price and arrive at the invoice price, pocket price and pocket margin after accounting for various deductions shown by the red bars.

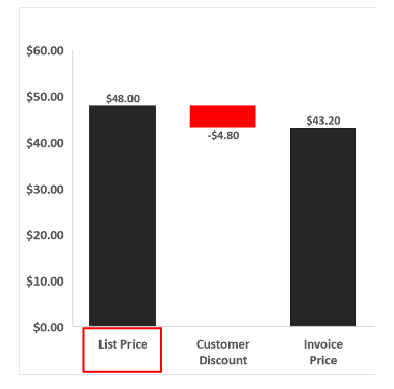

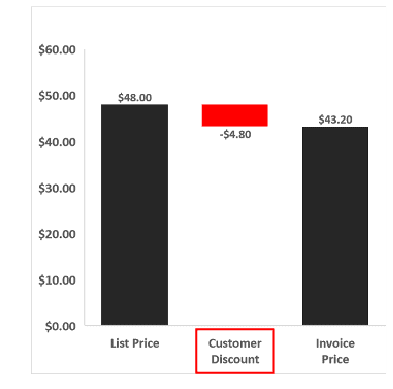

The List Price

Typically, the pricing structure for most companies begins with a reference price often labelled ‘List Price’ or ‘Base Price.’ The list price is the initial price set by the seller or manufacturer before any discounts, rebates, allowances or other deductions have been applied, and represents the maximum price a customer might pay. Also known as the ‘sticker price’ or the ‘manufacturer’s suggested retail price (MSRP), the list price is the starting point for building a price waterfall.

Customer Discounts

After the list price, the reductions that appear on the invoice are subtracted. Here we have deducted customer discounts. Those are customer-specific and set according to the relative size or importance of each customer. Examples of other discounts that may be placed after the list price include order size discounts or discounts in place of returns or warranty.

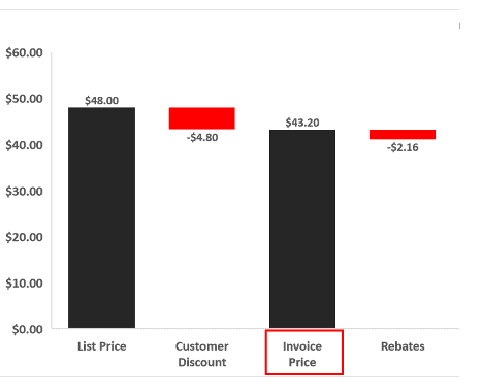

The Invoice Price

The Invoice Price is calculated by deducting discounts from the List Price. Although this is the price that customers make payments based on, it is not the amount that the seller receives as there are further allowances, discounts and rebates deducted from the invoice price.

Often managers will use the invoice price to understand their pricing strategy but that can lead to overlooked margin leakages.

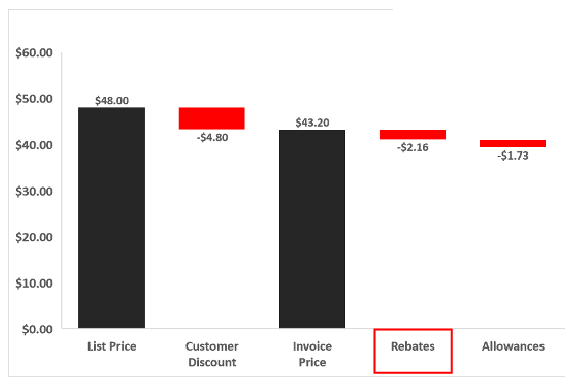

Office-Invoice Price Deductions

These are often referred to as “off-invoice price deductions” as they aren’t captured on invoice prices. Standard deductions include discounts for timely payments, marketing and partnership allowances, rebates related to distribution expenses and performance incentives such as sales and volume targets.

The Pocket Price

The pocket or net price represents the actual or net revenues generated from each transaction.

The Cost of Goods Sold

The COGs are directly attributable to goods produced by a company that have now been sold. In addition to production costs, COGs include the cost to serve a customer.

The Pocket Margin

This is the amount a company receives after subtracting COGs from the Pocket Price.

Keep Up With Market Size and Complex SKUs

Client Story Pricing Strategies for the Complex Environment of Aftermarket Service Parts Pricing Addressing complex product pricing, varying customer needs and values, and market share